Hello, budget-savvy friends! Today, we’re talking about the 50/30/20 rule. It’s a popular way to budget, but does it still work in today’s economic climate? With rising living costs, varying income levels, and diverse financial goals, some argue that the 50/30/20 rule might not be as relevant as it once was. Let’s dive in and find out together!

What is the 50/30/20 Rule?

First, let’s break down the 50/30/20 rule. It’s a simple way to divide your take-home income into three categories:

- 50% for needs: This includes essential expenses such as rent or mortgage payments, utilities, groceries, transportation, insurance, and any other necessary living costs.

- 30% for wants: These are discretionary expenses that enhance your lifestyle, such as dining out, entertainment, hobbies, travel, and shopping.

- 20% for savings or paying off debt: This portion goes towards building your financial future, including savings accounts, retirement funds, investments, and paying off debts like student loans or credit card balances.

So, why do people love this rule? It’s easy to understand and follow. It helps you balance your spending and saving without feeling too restrictive.

Pros of the 50/30/20 Rule

Let’s start with why this rule works well.

1. Simplicity

The 50/30/20 rule is easy to remember. Just three categories! It’s perfect if you’re new to budgeting. By simplifying your finances into three main categories, you avoid the overwhelming task of tracking every single expense. This makes it accessible for those who might find traditional budgeting methods too complex or time-consuming.

2. Flexibility

It allows for some fun! You get 30% for wants, so you don’t feel like you’re cutting out all the joy from your life. Many strict budgeting methods can make you feel deprived, leading to burnout and eventual abandonment of the budget. The 50/30/20 rule, however, encourages a balanced approach that includes room for leisure and enjoyment.

3. Balanced Approach

It helps you cover your needs, enjoy your wants, and save for the future. It’s a great way to start building good financial habits. By ensuring that all three major areas of your financial life are addressed, this rule helps promote long-term financial health and stability.

4. Promotes Savings

By allocating a fixed percentage to savings or debt repayment, the 50/30/20 rule encourages you to prioritize your financial future. This can be particularly helpful for those who struggle with saving consistently or who need to pay down significant debts.

Example 1: When It Works Well

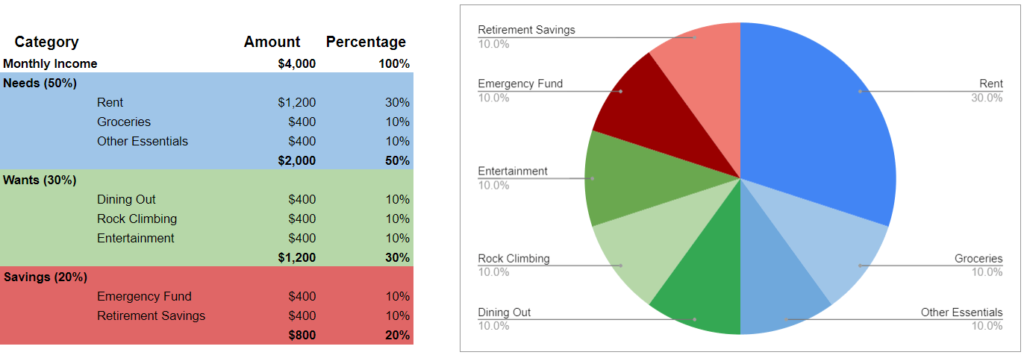

Let’s look at an example where this rule works perfectly. Meet Sara, a teacher in Austin, Texas. She likes rock climbing and going out with her friends. She earns $4,000 a month, and here’s how she applies the 50/30/20 rule:

- Needs (50%): $2,000

- Rent: $1,200 (30%)

- Groceries: $400 (10%)

- Other Essentials: $400 (10%)

- Wants (30%): $1,200

- Dining Out: $400 (10%)

- Rock Climbing: $400 (10%)

- Entertainment: $400 (10%)

- Savings (20%): $800

- Emergency Fund: $400 (10%)

- Retirement Savings: $400 (10%)

Budget Explanation

Sara’s monthly income is $4,000. Following the 50/30/20 rule, she allocates $2,000 for her needs. This includes $1,200 for rent, $400 for groceries, and $400 for other essentials like utilities and transportation. For her wants, she spends $1,200, divided into $400 each for dining out, rock climbing, and entertainment. Finally, she saves $800, splitting it equally between her emergency fund and retirement savings.

This breakdown fits her life perfectly and demonstrates how the 50/30/20 rule can be an effective budgeting tool for managing income, covering necessary expenses, enjoying life, and saving for the future.

Cons of the 50/30/20 Rule

But there are some reasons why it might not work for everyone.

1. Cost of Living

According to a 2023 study by the National Low Income Housing Coalition, about 30% of Americans live in high-cost areas where housing eats up more than 30% of their income. In cities like San Francisco, New York, and Los Angeles, rent alone can take up more than 50% of your budget.

High housing costs can make it nearly impossible to allocate only 50% of your income to needs, forcing you to either cut back drastically on wants and savings or to seek a different budgeting method that better suits your situation.

Example 2: When It Doesn’t Work Well

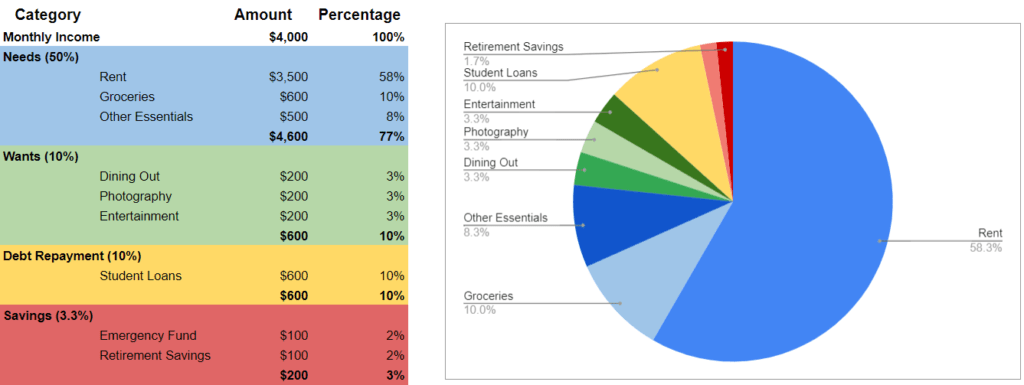

Now, let’s consider an example where the 50/30/20 rule doesn’t quite fit. Meet Mike, a freelance graphic designer living in San Francisco. He earns around $6,000 a month, but his income can vary. Mike enjoys photography as a hobby, often spending weekends capturing the vibrant cityscape. Additionally, he has some student loans he’s paying off. Here’s how his budget looks:

- Needs (76.7%): $4,600

- Rent: $3,500 (58.3%)

- Groceries: $600 (10%)

- Other Essentials: $500 (8.4%)

- Wants (10%): $600

- Dining Out: $200 (3.3%)

- Photography Equipment and Supplies: $200 (3.3%)

- Entertainment: $200 (3.3%)

- Debt Repayment (10%): $600

- Student Loans: $600 (10%)

- Savings (3.3%): $200

- Emergency Fund: $100 (1.7%)

- Retirement Savings: $100 (1.7%)

Budget Explanation

Mike’s total monthly income is $6,000. However, his rent alone is $3,500, which consumes 58.3% of his income, far exceeding the 30% suggested by the 50/30/20 rule. When we add his groceries at $600 and other essentials at $500, his total spending on needs rises to $4,600, which is 76.7% of his income. This leaves only $1,400 for his wants, debt repayment, and savings.

For his wants, he allocates $200 each to dining out, photography equipment and supplies, and entertainment, totalling $600. This is just 10% of his income, less than the recommended 30%. Mike also dedicates $600 (10%) towards repaying his student loans.

For savings, he puts aside $200, split equally between his emergency fund and retirement savings, accounting for just 3.3% of his income.

In high-cost living areas like San Francisco, adhering strictly to the 50/30/20 rule can be challenging. With the addition of debt repayment, balancing needs, wants, and savings becomes even more difficult. In such situations, a more flexible budgeting approach is necessary to accommodate higher living costs and debt obligations while still striving to maintain financial stability. If he really wants to follow the 50/30/20 budgeting method, he should look at increasing his income or ways to reduce his rent.

2. Income Variability

Over 40% of Americans have variable incomes due to gig work, freelancing, or seasonal jobs, as reported by a 2022 study from the Federal Reserve. This makes it hard to stick to fixed percentages because your income changes each month.

For those with irregular income, setting aside fixed percentages for needs, wants, and savings can be challenging. Instead, these individuals might benefit from a more dynamic budgeting approach that adjusts based on their actual earnings each month.

3. Personal Goals

Everyone’s financial situation is different. Maybe you need to save more aggressively, or you have less debt to pay off. For instance, someone working towards early retirement might want to allocate a larger portion of their income to savings and investments, while someone with minimal debt might focus more on discretionary spending and enjoying life.

Example 3: When It Works with Adjustments

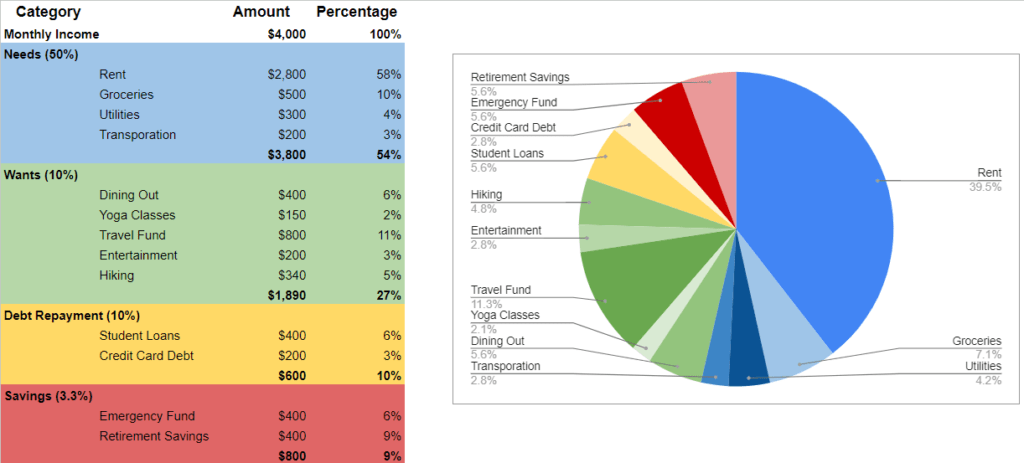

Finally, let’s explore an example where the 50/30/20 rule works with a few adjustments. Meet Emma, a software engineer living in Toronto. She earns $7,000 a month and enjoys yoga and hiking. Emma’s budget looks like this:

- Needs (54.3%): $3,800

- Rent: $2,800 (40%)

- Groceries: $500 (7.1%)

- Utilities: $300 (4.3%)

- Transportation: $200 (2.9%)

- Wants (27.1%): $1,890

- Dining Out: $400 (5.7%)

- Yoga Classes: $150 (2.1%)

- Travel Fund: $800 (11.4%)

- Entertainment: $200 (2.9%)

- Hiking Gear: $340 (4.9%)

- Savings (11.4%): $800

- Emergency Fund: $400 (5.7%)

- Retirement Savings: $400 (5.7%)

- Debt Repayment (8.6%): $600

- Student Loans: $400 (5.7%)

- Credit Card Debt: $200 (2.9%)

Budget Explanation

Emma’s total monthly income is $7,000. Her rent is $2,800, which takes up 40% of her income. Adding groceries at $500, utilities at $300, and transportation at $200, her total spending on needs comes to $3,800, or 54.3% of her income. This is slightly above the recommended 50% but manageable.

For her wants, Emma allocates $400 to dining out, $150 to yoga classes, $800 to her travel fund, $200 to entertainment, and $340 to hiking gear, totaling $1,890 or 27.1% of her income. This is a bit lower than the recommended 30% but allows her to enjoy her interests.

Emma also saves $800 monthly, split equally between her emergency fund and retirement savings, accounting for 11.4% of her income. She puts $400 each into these two savings categories.

Lastly, she allocates $600, or 8.6% of her income, towards repaying her debts. This includes $400 for student loans and $200 for credit card debt.

To make the 50/30/20 rule work for her, Emma has adjusted her categories slightly. By reducing her wants to 27.1% and her savings to 11.4%, she can cover her higher-than-average needs expenses while still saving and enjoying her lifestyle. Additionally, Emma takes on occasional freelance projects to boost her income, making it easier to stick to her budget.

This example demonstrates that while the 50/30/20 rule is a great starting point, it’s important to adjust it based on your individual circumstances and goals. Emma’s adjustments allow her to balance her needs, wants, and savings in a way that works for her, proving that flexibility is key in budgeting.

Customizing the 50/30/20 Rule

It’s important to remember that budgeting is personal. The 50/30/20 rule is a great guide, but it’s okay to adjust it. Here are some tips on how to customize this rule to fit your lifestyle and financial goals better.

1. Adjust the Percentages

If your needs take up more than 50% of your income due to high living costs, you might allocate 60% to needs, 20% to wants, and 20% to savings. Alternatively, if you want to save more aggressively, you could adjust to 40% needs, 20% wants, and 40% savings.

2. Create a Buffer

For those with variable incomes, creating a buffer or emergency fund can help manage the fluctuations. Allocate a portion of your income to this fund during high-earning months to cover expenses during lower-earning months.

3. Focus on High-Priority Goals

If you have specific financial goals, such as buying a house or paying off a large debt, adjust your budget to prioritize these goals. This might mean temporarily allocating a larger percentage of your income to savings or debt repayment.

Final Thoughts

So, does the 50/30/20 rule still work? Yes, but it depends on your situation. It’s a fantastic starting point, especially if you’re new to budgeting. But don’t be afraid to change it to fit your life. The most important thing is to have a budget that works for you.

By understanding the basics of the 50/30/20 rule and how to customize it, you can create a budget that meets your unique financial needs and goals. Remember, the key to successful budgeting is flexibility and adaptability. Your financial situation will change over time, and your budget should evolve with it.

If you found this blog post helpful, please subscribe for more tips on taking control of your finances. And if you have any questions or topics you want me to cover, drop them in the comments below. Let’s keep budgeting smarter together!